How Private Credit Thinks About Distressed Opportunities vs. How Advisors Think About Restructuring

There’s a subtle but important disconnect in how people talk about “distress." Alpha isn’t about picking a side, it's about knowing when to flip

I’m not sure if you’re aware by now but I love diving into the nuances of how different players in the ecosystem approach the same messy situations. So, I decided I’m gonna unpack something that’s been on my mind a lot lately i.e. the divide between how private credit investors eye distressed opportunities and how restructuring advisors navigate the actual process. It’s subtle, but once you see it, it changes how you think about deals, incentives, and even your own career path.

I first noticed this gap during a late-night chat with a colleague at a conference last year. We were debating a high-profile bankruptcy case, and it hit me investors are all about the upside in chaos, while advisors are laser-focused on herding cats through the storm without getting scratched. If you’re in private credit, restructuring advisory, or just curious about the credit markets, this one’s for you. I’m going to break it down step by step (frankly if you have a bad attention span, you might wanna click out because this’ll take about 8-9 mins of me just going on and on).

First, What Am I Even Talking About

Distressed situations arise when a company hits the skids maybe it’s overleveraged, facing liquidity crunches or slammed by market shifts like tariffs, the energy transition, AI disruption or lingering supply chain woes. Private credit, that booming industry now exceeding $2 trillion in AUM (per Moody’s 2026 outlook, with projections approaching $4 trillion by 2030), has become a dominant player. These direct lenders, funds like Ares, Apollo, Blackstone Credit, provide loans outside traditional banks, often to middle-market companies with tighter covenants and more lender control. On one side, private credit folks underwrite with an eye toward distress from day one. On the other, advisors like investment bankers from PJT Partners or Houlihan Lokey, lawyers from Kirkland & Ellis, or turnaround consultants like AlixPartners step in when things tip over to manage the workout. The magic (and the friction) happens where their worlds collide i.e. incentives, timelines and risk appetites that don’t perfectly align.

Why now? As we hit early 2026, defaults are ticking higher. Fitch forecasts U.S. leveraged loan defaults at 4.5-5% for the year, while S&P sees speculative grade corporates easing to 4% by September (down from 4.6% in 2025, but still elevated). Interest coverage has compressed to ~1.5x in stressed pockets (down from 3.2x peaks in 2021, with 47% of borrowers below 1.5x), PIK toggles are more common (now 8% of public BDC investment income), and failed liability management transactions (LMTs) are leading to more change-of-control handovers. Understanding these lenses isn’t nerdy, it’s deal-making edge in a market where opportunistic funds have raised $100B+ for distress plays.

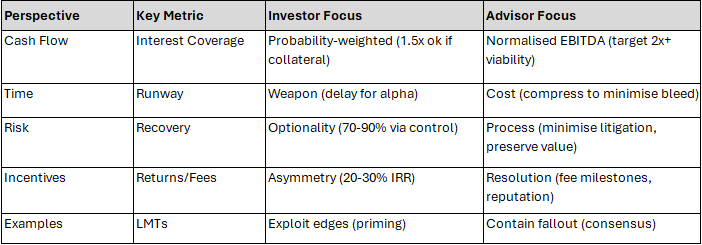

How Private Credit Thinks About Distressed Opportunities

Private credit investors don’t wait for distress. Underwriting prioritises downside protection, maintenance covenants on leverage ratios (often 5-6x net debt/EBITDA), anti-hoarding provisions or sacred rights that block junior debt incursions or force asset sales. In a normal deal, it’s about yield (SOFR + 500-700 bps, sometimes pushing 800+ in riskier pockets) but in distress, it’s an opportunity. They spot undervalued assets or mispriced risk where banks won’t touch, think collateral like IP in tech (valued at 2-3x book) or real estate in retail (often covering 1.5-2x exposure).

For example, in a distressed play, private credit might swoop in with debtor-in-possession (DIP) financing, super-senior loans at SOFR + 800-1000 bps, often with equity conversion rights. I think I talk a lot about Hertz in 2020, but that’s cuz it remains the classic, Apollo’s DIP turned into ownership stakes post-reorg. Fast-forward to 2025, with covenant-lite loans (now ~85% of the market, up from 70% pre-pandemic), investors got creative with loan-to-own strategies, buying debt at 60-70 cents on the dollar and pushing for control. Take Tricolor’s 2025 bankruptcy, private lenders like Apollo and Oaktree stepped in on auto loan portfolios, leveraging collateral to recover 80-90% while juniors got crammed down. But here’s the human side, investors thrive on asymmetry. They’re patient capital with 5-7+ year horizons, so they can afford to play the long game. I’ve chatted with PMs who say, “Distress is where alphas are made; buy low, restructure, exit high.” Their incentive? Carried interest on outsized returns (20-30% IRRs in strong plays vs 10-15% in performing). Risk? Sure, but mitigated by deep due diligence, stress-testing recoveries at 50-70% on collateral. Yet it’s not all rosy. In a crowded market (dry powder at $150B+ for Ares alone), competition from hedge funds inflates prices, turning “opportunities” into traps. And let’s be real, ego plays a role. Some investors get starry-eyed about being the white knight only to face brutal negotiations in fractured lender groups.

Cash Flow is important but Control is more important

Advisors spend a lot of time modeling normalised EBITDA, sustainable capex and long term viability. Private credit cares about those too but only insofar as they affect liquidity runway, ability to enforce and probability weighted recovery. A distressed credit deal can work even if the business shrinks, EBITDA never recovers, or the equity is wiped out. As long as the investor is senior enough, has collateral or structural protections, and can influence timing and outcomes. This is why private credit is comfortable backing companies that look ugly as long as the capital structure is uglier.

Okay think about it: In a scenario where cash flow is sputtering (interest coverage dipping to 1.2x), private credit isn’t fixated on turning the ship around to blue-sky projections (e.g. 15% EBITDA margins). They’re okay with a controlled descent if it means they land with the assets. I’ve seen deals where lenders step in on underperforming retail chains, not because they believe in a comeback story, but because the real estate collateral covers their exposure twice over. Control trumps cash flow because it lets them dictate the narrative, whether that’s forcing a 363 sale, amending terms (e.g. PIK toggle to defer cash pay), or priming other creditors via super-senior facilities.

The most underappreciated part of distressed private credit is how much of the return comes from embedded options, not coupons. Like convert-to-equity rights, step-up pricing post restructuring, call protection plus equity kickers (5-10% stubs), ability to credit bid in a sale (bypassing auctions) or amend-and-extend fees (1-2% upfront) layered on existing exposure. Advisors model base cases but Private credit models decision trees: What happens if the deal is consensual (80% probability, 25% IRR)? Delayed (15% prob, 18% IRR)? Goes to court (5% prob, 12% IRR with litigation costs)? Assets sold (quick 1x MOIC)? Sponsor walks (equity handover)? Distress is valuable because it creates paths, not certainty. in 2025, opportunistic funds capitalised on this, raising $100B+ for volatility plays.

In my experience, this optionality is where the magic happens. For instance, in one energy deal I followed, lenders built in warrants that kicked in if oil prices stayed low, effectively giving them upside without upfront dilution. Or in tech, where IP collateral allows for credit bids that turn debt into ownership. It’s not about the 10-12% coupon, it’s the 2-3x multiple from those hidden levers. Private credit loves this because funds are structured for illiquidity premiums (8-10% over public), turning time and complexity into alpha. But watch out rising PIK toggles (up 28% YoY in BDCs) signal stress, masking cash shortfalls.

How Advisors Think About Restructuring

Flip the script to advisors and it’s a different vibe. These are the fixers, brought in by the company (or sometimes creditors) to orchestrate the chaos. Their lens? Process risk, the myriad ways a restructuring can derail, from creditor infighting to regulatory hurdles. Advisors start with triage: Assessing the capital structure, modeling scenarios (Chapter 11, out-of-court exchange, or sale), and mapping stakeholders. Unlike investors, they’re not betting their own money, they’re fee-based, often on success milestones. A big restructuring can net millions in advisory fees, but only if it closes smoothly. Key tools in their kit is Creditor committees, where they negotiate haircuts, equitisations or new money infusions. They manage timelines, think 120 day exclusivity periods in bankruptcy to keep momentum. Risk management is paramount. Advisors stress over “process leaks” like leaks to the press sparking runs on suppliers or employee exodus.

Take the recent Bed Bath & Beyond saga (which dragged into 2023-24). Advisors like AlixPartners helped carve out assets for sale while fending off activist creditors. Or in energy, post-OPEC+ volatility, firms like Lazard have steered oilcos through liability management transactions (LMTs), swapping debt to extend maturities without full consents. Take the 2025 First Brands; advisors like Lazard carved assets for sale while fending activists, but underwriting lapses (overvalued auto parts) led to bankruptcy. Tricolor in autos; AlixPartners steered LMTs swapping debt, extending maturities without full consents amid 1.2x coverage.

From my chats with advisors, their mindset is pragmatic: “Control the narrative, align incentives, minimise litigation.” They’re kinda like diplomats often dealing with emotional boards or aggressive hedge funds. Incentives? Billable hours and reputation, but if you botch a process, your next mandate dries up. But diverge from investors? Absolutely. Advisors push for holistic solutions that preserve enterprise value, even if it means diluting seniors or cram downs on juniors. It’s exhausting though. Advisors live in the trenches of endless calls, red-eye flights, modeling till dawn. One time I was told, “Investors dream of home runs; we just want no strikeouts, honeybutter”

A “good” restructurin from an advisor’s lens is one that preserves enterprise value (80-90% recovery), avoids uncontrolled outcomes, minimises litigation and keeps stakeholders at the table. This is rational. Advisors are judged on whether the company survives, whether the process stays orderly and whether outcomes are defensible ex-post. They are not paid for asymmetry but for the resolution. In practice, this means advisors prioritise deals that look “clean”, meaning pre-packs where everyone’s on board or out-of-court exchanges that dodge bankruptcy altogether. They’re the ones calming the room when tensions flare, ensuring that value doesn’t evaporate in endless fights.

For private credit, time can be a weapon. For advisors, time is almost always a liability. This is why advisors push for early engagement, standstills, waivers and pre-packaged or pre-negotiated solutions. They are trying to collapse uncertainty. Private credit is often trying to price it. I’ve witnessed this in real time, advisors racing against the clock in a manufacturing turnaround, securing waivers to buy a few months while negotiating. Delay means more fees, sure, but also higher risk of total collapse. Advisors are deeply conscious of intercreditor dynamics, pari passu treatment, legal defensibility and “reasonableness” of outcomes. Private credit does not ignore these but it is far more willing to exploit edges that exist within the rules. That’s not cynicism, it’s fiduciary duty. If a structure allows super-senior priming, non-pro rata amendments, liability management exercises or drop-downs or asset segregation, private credit will at least analyse it. Advisors will usually try to contain it, fearing it sparks litigation or alienates key players.

Broader 2026 implications: Rising stress (PIK up, coverage down, failed LMTs to handovers) amplifies clashes. Private credit growth (rivaling HY bonds at $1.5T) crowds advisors, but enables orderly paths.

Why This Matters If You Care About Distressed Investing

If you want optionality into distressed private credit, this distinction matters more than technical modeling. Senior people can tell very quickly whether you think like a process manager or think like a capital allocator. The best investors understand both but they are clear-eyed about which hat they are wearing. They know when to support stability and when to benefit from instability. They respect advisors and also understand why their incentives will never fully align.

The real edge is knowing which language to speak. The mistake many early-career professionals make is trying to sound “balanced” all the time. The people who stand out know when to talk about fairness, when to talk about control, when to talk about value and when to talk about outcomes. They don’t confuse good processes with good investments. And they don’t confuse good investments with good optics. Distress lives in that tension. If you can articulate it clearly (without moralising it) you signal something rare i.e. you don’t just understand restructuring, you understand why capital behaves the way it does when things break. That’s the real skill.

More clashes ahead in Big 2026 (but big opportunities in a split market)

Looking ahead to the rest of 2026, the private credit market feels like a classic K-shaped recovery. Just picture the letter K: one leg shoots up strong (the winners keep winning) while the other leg drags down (the weaker players struggle hard). It’s not a uniform boom or bust, it’s bifurcation, where the market splits into haves and have-nots. Strong, high-quality borrowers like think companies with solid margins, good cash flow, or ties to hot sectors like AI/data centers, can refinance their loans at relatively attractive rates (around SOFR + 400-500 basis points, or roughly 8-9% all-in yields). They keep growing, maybe even expand via acquisitions. But weaker borrowers, especially those in low-margin industries, super-sensitive to interest rates, or already stretched on debt, hit real walls. Liquidity dries up, payments get tough, and restructurings kick in.

What we’re likely to see more of (personal views only):

Change-of-control deals from failed liability management transactions (LMTs). Remember the aggressive moves in 2025 cases like Altice or KIK? Those “creative” tactics (shifting assets, non-pro rata changes) bought time but often backfired when lenders pushed back. In 2026, expect more sponsors or owners “handing over the keys” to lenders and basically saying, “we can’t fix this, you take control.” This creates fresh opportunities for private credit funds to step in, restructure, and potentially own pieces of the company post-workout.

More workouts in the middle market (companies typically $50M-$500M in revenue). KBRA’s January 2026 outlook projects direct lending defaults rising to about 2% by volume (up from 1.5% in 2025), still manageable thanks to strong covenants and lender workout skills, but a clear uptick from declining growth, higher leverage and maturing loans in certain segments. Private credit’s smaller lender groups (often just 3-5 players vs. dozens in public markets) usually mean quicker, more consensual fixes, so no endless court battles.

Opportunistic plays in asset based finance (ABF). This is lending backed by real assets like consumer loans, equipment, mortgages, or even royalties. Think cash flows from stuff the company owns, not just future profits. Ares highlights a massive $28 trillion addressable market here, and Moody’s sees ABF as the fastest-growing slice of private credit in 2026. As banks pull back from riskier lending, private credit fills the gap with higher yields, better protections and less volatility than pure corporate bets.

Covenant erosion (now ~85% of loans are “covenant-lite” meaning fewer strict rules) adds some volatility. Lenders have less early warning levers but the smaller, more nimble lender clubs still favor fast resolutions over drawn out fights.

A big wildcard in my opinion is the interest rates. If they stay “higher for longer” (Fed funds likely hovering around 3.5-4%, with markets pricing limited cuts this year amid sticky inflation and solid jobs data), companies keep feeling the pinch. PIK toggles (payment-in-kind, where interest gets added to the loan balance instead of paid in cash) are already rising, buying short-term breathing room but piling up bigger problems later. Watch business development companies (BDCs), they’re among the most transparent parts of private credit, so spikes in PIK income or non-accruals often signal broader asset-quality cracks early.

Bottom line for 2026 (in my dramatic ass opinion) is more tension between investors and advisors (clashes over aggressive terms, late rescues, or re-ranking debt), but also real alpha in selectivity. The market rewards those who spot the bifurcation early, bet on quality collateral, control-oriented structures and ABF growth while avoiding the truly stressed pockets. It’s not a crisis year but a test of discipline for who can navigate the split economy without getting caught in the down leg.

Wrapping it up

So there you have it, the investor’s opportunistic lens vs the advisor’s procedural shield. Both essential, but incentives pull apart, creating friction that forges better deals or blows them up. If you’re in the game, my advice would be to talk across the divide. For investors, appreciate the process grind; for advisors, grasp the return math.

Moral of the story? In distress, the real alpha is knowing whose side you’re secretly rooting for… and when to switch teams lol